Blast from my past: "Asia: The Military-Market Link" (2002)

Asia: The Military-Market Link

by

Thomas P.M. Barnett

China could be the world's largest auto market by 2020, increasing its oil needs by 40%. The Pentagon and Wall Street must understand their interrelationship: economic and political stability are crucial to reducing energy market risk.

COPYRIGHT: The U.S. Naval Institute, 2002 (January issue, pp. 53-56); reprinted with permission

There is a real push within the Department of the Navy to enunciate the presumed linkage between the Navy’s worldwide operations and economic globalization. Some of this analytic effort is dismissed as pouring old wine into new wineskins, because many Navy-as-the-glue-of-globalization formulations sound an awful lot like the old bromides about the “Navy as the glue of Asia.” Nice work if you can get it, but given the relative lack of naval crisis response in Asia since the end of the Vietnam War, it is a hard story to sell.

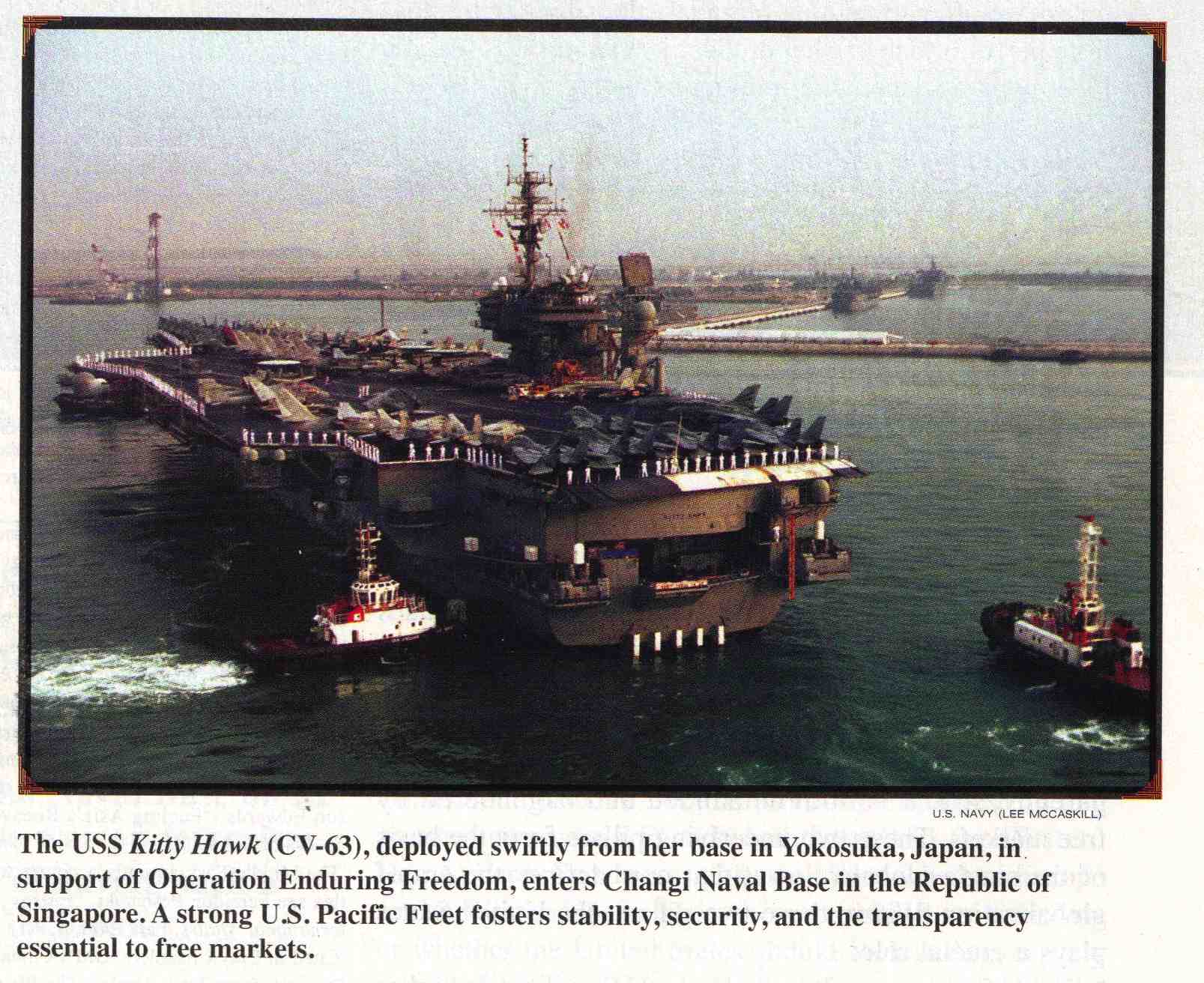

But all that is about to change, if you believe the Department of Energy’s stunning projections of Asia’s growing energy consumption over the next 20 years.1 Because to ensure the region’s much-anticipated economic maturation, a lot of good things must occur over the next two decades in both Asia and the Middle East—and across all paths in between.2 In short, if you want a Pacific Century, you’ll need a U.S. Pacific Fleet—strong in numbers and forward deployed.

Asian Energy: A Globalization Decalogue

As the director of a long-running Naval War College project (NewRuleSets.Project) on how globalization alters definitions of international security, I have had the opportunity to spend a lot of time with Wall Street executives and regional security experts (both military and civilian) discussing Asia’s future economic and political development.3 The following decalogue distills the essential rule sets our project has identified concerning Asia’s energy future.4

1. The Global Energy Market Has the Necessary Resources.

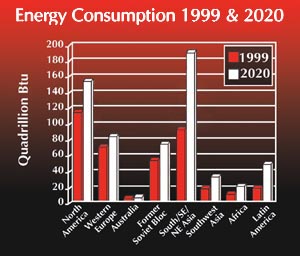

Asia as a whole currently uses about as much energy as the United States, or almost 100 quadrillion British thermal units (Btu).5 By 2020, however, Asia will roughly double its energy consumption while U.S. consumption rises just more than 25%. Asia’s likely increases are significant no matter what the energy category:

- Oil, 88%

- Natural gas, 191%

- Coal, 97%

- Nuclear power, 87% when Japan is included, 178% when it is not

- Hydroelectricity and other renewables, 109%.

This is a genuine changing of the guard in the global marketplace—a shifting of the world’s demand center. Today, North America accounts for just under a third of the world’s energy consumption, with Asia second at 24%. Within one generation, those two regions will swap both global rankings and percentage shares (see chart).

The good news is that there’s plenty of fossil fuel to go around. Confirmed oil reserves have jumped almost two-thirds over the past 20 years, according to the Department of Energy, while natural gas reserves have roughly doubled. Our best estimates on coal say we have enough for the next two centuries. So supply is not the issue, and neither is demand, leaving only the question of moving the energy from those who have it to those who need it—and therein lies the rub.

2. But No Stability, No Market.

Asia comes close to self-sufficiency only in coal, with Australia, China, India, and Indonesia the big producers. All told, Asia self-supplies on coal to the tune of 97%, a standard it will maintain through 2020. That is important, because virtually all of the global growth in coal use over the next generation will happen in Asia, mostly in China and India.

Natural gas is a far different story. In 2001 Asia used around 10 trillion cubic feet, with Japan, South Korea, and Taiwan representing the lion’s share of consumption. The trick is this: Asia’s demand for natural gas will skyrocket to perhaps 25 trillion cubic feet by 2020, with the vast bulk of the increase occurring outside of that trio. So if those three countries already buy what’s available in-region, that means the rest of Asia will have to go elsewhere—namely, the former Soviet Union (Russia, with 33% of the world total) and the Middle East (Iran, with 16%).

Finally, even though oil will decline as a percentage share for Asia as a whole over the coming years, absolute demand will grow by leaps and bounds. Asia currently burns about as much oil as the United States, or roughly 20 million barrels per day (mbd). Since oil is mostly about transportation nowadays, and Asia is looking at a quintupling of its car fleet by 2020, there is a huge swag placed on this projection. The Department of Energy’s latest forecast is roughly 36 mbd, but even that means Asia as a whole has to import an additional 12 mbd from out of region, or roughly double what it imports today from the Persian Gulf region.6

Asia already buys roughly two-thirds of all the oil produced in the Persian Gulf, and by 2010 that share will rise to approximately three-quarters.7 Meanwhile, the West’s share of Gulf oil will drop from just under a quarter today to just over a tenth in 2010. Strategic upshot? The two most anti-Western corners of the globe are inexorably coming together over energy and money. Increasingly, the Middle East becomes dependent on economic stability in Asia, and Asia becomes dependent on political-military stability in the Gulf. If either side of that equation fails, the energy market is put at risk.

3. No Growth, No Stability.

As a middle class develops in Asian countries, a significant portion of the global population is being rapidly promoted from an 18th- or 19th-century lifestyle into a 20th- or even 21st-century consumption pattern. If international investors decide to take it all away one afternoon in a flurry of currency attacks and capital flight, the struggling segment of the population that suddenly finds itself expelled from the would-be middle class is likely to get awfully upset.

4. No Resources, No Growth.

Asia cannot grow without a huge influx of out-of-area energy resources. The quintupling of cars is impressive enough, when you consider that General Motors predicts China will be the world’s largest car market in 2020.8 But even more stunning will be the 250% increase in electricity consumption (300% in China), which will be generated mostly by coal and, increasingly, natural gas. Put those two together and we are talking about an Asia that must open up to the outside world to a degree unprecedented in modern history.

5. No Infrastructure, No Resources.

Asia’s infrastructure requirements over the next two decades are unprecedented. The combination of a doubling in energy consumption and rapid rises in population, urbanization, and water usage will damage further an already battered regional ecosystem, placing great political pressures on national governments to limit the pollution associated with energy production.

In Asia, the push for energy is really a push for infrastructure, which comes in three forms:

- For the near term, the vast majority of natural gas that flows into Asia will arrive in a liquid form on ships. That means port facilities on both ends of the conduit, plus liquefaction plants on the supplier’s end and regasification plants on the buyer’s end.

- Over the longer haul, pipelines by both land and sea become the answer to meeting the rising demand.

- Finally, there is the domestic infrastructure required to pipe all that gas to the final consumers.

None of this comes cheaply, and as the recent history of regional electricity development makes clear, lots of outside money is required.9

6. No Money, No Infrastructure.

Foreign direct investment (FDI) is the most significant scenario variable for Asia’s energy future. Asia’s energy infrastructure requirements easily will top $1 trillion by 2020, according to many estimates. Such numbers overwhelm the region’s ability to self-finance, and that means Asia will have to open up its energy generation and distribution markets to far more joint or foreign ownership. If it seems inevitable that Asia must turn to the former Soviet Union and the Middle East for energy in the coming decades, it is just as inevitable that it must turn to the West for the money to finance this trade.

7. No Rules, No Money.

Many on Wall Street voice the opinion that Asia has not sufficiently cleaned up its act as a result of the 1997–1998 financial crisis, referring primarily to internationally accepted accounting practices in the financial and corporate sectors.10 Another problem with Asia’s energy investment climate is the current mix of private-sector investments and public-sector decision making. In most Asian economies, the government still plays far too large a role as far as Western financiers are concerned. As long as rule sets lag behind, the rise of private-sector market makers is delayed, for firm rules of play are required before deregulation of state-run energy markets can proceed.

8. No Security, No Rules.

Foreign direct investment does not occur in a vacuum. Long-term certainty is the greatest attraction a country can offer to outside investors, whereas war and political-military instability (especially leftist revolutions) are the best methods to scare them away. Developing Asia readily presents a handful of potential and/or existing security trouble spots that could negatively affect the region’s FDI climate in significant ways.

9. No Leviathan, No Security.

Many international experts agree that Asia’s current security situation belongs to what Thomas Friedman calls the “olive tree” world, where backward tribes fight over little bits of land, while rising economic powerhouses clearly join the “Lexus” world, producing many of the global economy’s best high-end technology products.11

In this region there remains a viable long-term market for the services of an outside Leviathan—namely, the United States. The United States enjoys healthier security relationships with virtually every Asian government than any two governments there enjoy with one another. While it is easy to deride the notion of a “four-star foreign policy,” there is little doubt that the commander-in-chief of U.S. Pacific Command plays a unique role in working the security arrangements that underpin the region’s strong record of structural stability over the past quarter century.12 Our forward presence both reassures local governments and obviates their need for larger military hedges. Our presence is a moneymaker on two fronts: they spend less on defense and more on development (the ultimate defense), and FDI is encouraged, however subtly.

10. No U.S. Navy, No Leviathan.

The U.S. government—and the U.S. Navy in particular—faces a far more complex strategic environment in the 21st century than it did during the Cold War, whether or not it yet realizes the change: our national security interests in the Persian Gulf, while increasingly important for the global economy, no longer hold the same immediate importance to our national economy. In effect, U.S. naval presence in Asia is becoming far less an expression of our nation’s forward presence than an “exporting” of security to the global marketplace. In that regard, we truly do move into the Leviathan category, for the “product” we provide is increasingly a collective good less directly tied to our particularistic national interests and far more intimately wrapped up with our global responsibilities.

And in the end, this is a pretty good deal. We trade little pieces of paper (our currency, in the form of a trade deficit) for Asia’s amazing array of products and services. We are smart enough to know this is a patently unfair deal unless we offer something of great value along with those little pieces of paper. That product is a strong U.S. Pacific Fleet, which squares the transaction nicely.

Understanding the Military-Market Connection

The collapse of the Soviet bloc and its long-standing challenge of the Western economic rule set made possible a global rule set for how military power buttresses and enables economic growth and stability. For the first time in human history we have a true global military Leviathan in the form of the U.S. military, and no peer competitor in sight—not even a coherent alternative economic philosophy (although bin Laden’s anti-Westernization resonates with those who fear globalization as a form of forced Americanization). This unparalleled moment in global history both allows and compels the United States to better understand the national security-market nexus.

How do we define this yin-yang relationship between business and the military? First we speak of stability, which flows from national security, and then we speak of transparency, which is both demanded and engendered by free markets. These two underlying pillars form the basis of the single global rule set that now defines the era of globalization. Within those two pillars, the United States plays a crucial role:

- The U.S. government, through the U.S. military, supplies the lion’s share of system stability through its Leviathan-like status as the world’s sole military superpower.

- U.S. financial markets, which lead the way in fostering the emergence of a global equities market, play the leading role in spreading the gospel of transparency—any country’s best defense against the sort of financial currency crises that have erupted periodically over the past decade (Mexico 1994, Asia 1997, Russia 1998, Brazil 1999, Turkey 2001).

It therefore is essential that the Pentagon and Wall Street come to better understand their interrelationships across the global economy. Uncovering and better understanding this fundamental relationship is especially important because the vast majority of the time the security and financial communities operate in oblivious indifference to one another. Ultimately, however, the global economy operates on trust, which is based on certainty, which in turn comes from the effective processing of risk.

In the end, the national security and financial establishments are in the same fundamental business: the effective processing of international risk. Invariably, these two problem sets merge in the historical process that is economic globalization. Understanding the military-market connection isn’t just good business, it’s good national security strategy. Bin Laden understood this connection when he selected the World Trade Center and the Pentagon for his targets. We ignore his logic at our peril.

1. See the Energy Information Administration’s International Energy Outlook 2001, DOE/EIA-0484(2001), March 2001, found at www.eia.doe.gov/oiaf/ieo/index.html.

2. For the purposes of this article I define Asia as extending from Afghanistan to Japan, but not including Australia and New Zealand (Oceania), although I identify Australia as an in-region supplier of energy because of its proximity.

3. The NewRuleSets.Project is a multiyear research effort designed to explore how globalization and the rise of the new economy are altering the basic “rules of the road” in the international security environment, with special reference to how these changes may redefine the U.S. Navy’s historical role as security enabler of U.S. commercial network ties with the world. The project is hosted by the online securities broker-dealer firm eSpeed (an affiliate of Cantor Fitzgerald LP) and involves personnel from the Decision Strategies Department of the Center for Naval Warfare Studies. Adm. William Flanagan, USN (Ret.), and Dr. Philip Ginsberg, of Cantor Fitzgerald (senior managing director and executive vice president, respectively), serve as informal advisors to the project, actively participating in all planning and design. The first three joint Wall Street-Naval War College workshops in the series involved energy, foreign direct investment, and the environment in Asia. Follow-on events are planned for food and water, information technology, and human capital. All research products relating to this effort are found at www.nwc.navy.mil/newrulesets.

4. All the energy data presented in the decalogue, unless otherwise specified, comes from the Department of Energy’s International Energy Outlook 2001.

5. A good rule of thumb for thinking about quadrillion Btu is that you can take the annual number for a region, divide it by two, and get the rough equivalent in millions of barrels of oil per day the region would need to burn if it was achieving that entire energy amount by oil alone. For example, North America used 116 quadrillion Btu in 1999, which would equate to 58 million barrels of oil per day (mbd) if that entire amount was achieved by oil alone. For point of comparison, the United States currently uses about 20 mbd, importing roughly half that number.

6. For an excellent exploration of this, see Daniel Yergin, Dennis Eklof, and Jefferson Edwards, “Fueling Asia’s Recovery,” Foreign Affairs, March/April 1998, pp. 34–50.

7. The Middle East currently accounts for roughly 90% of all Asian oil imports; on this see Fereidun Fesharaki, “Energy and Asian Security Nexus,” Journal of International Affairs, Fall 1999, p. 97.

8. Cited in Clay Chandler, “GM’s China Bet Hits Snag: WTO (Car Shoppers Await Discount from Trade Deal),” The Washington Post, 10 May 2000, p. E1.

9. See “Foreign Investment in the Electricity Sectors of Asia and South America,” International Energy Outlook 2000, pp. 120–21.

10. On this, see Andreas Kluth, “A Survey of Asian Business: In Praise of Rules,” The Economist, 7 April 2001, pp. 1–18 (insert).

11. Thomas Friedman, The Lexus and the Olive Tree: Understanding Globalization (New York: Farrar Strauss Giroux, 1999).

12. For an excellent exploration of this concept, see Dana Priest, “A Four-Star Foreign Policy? U.S. Commanders Wield Rising Clout, Autonomy,” The Washington Post, 28 September 2000, p. A1. See also the second and third articles in the series (29–30 September).

Dr. Barnett is a professor at the U.S. Naval War College, currently serving as the Assistant for Strategic Futures in the Office of Force Transformation within the Office of the Secretary of Defense.

Thomas P.M. Barnett

Thomas P.M. Barnett

Reader Comments