![]()

Foreign Direct Investment:

Decision Event Report II of the

NewRuleSets.Project

by

Dr. Thomas P.M. Barnett

with

Prof. Bradd C. Hayes

and inputs from

Dr. Lawrence Modisett

Cdr. Carl Carlson, USN

Prof. Gregory Hoffman

18 May 2001 final draft

Contents

I. Project overview and introduction

II. The Asian Energy Futures key findings

III. The Foreign Direct Investment workshop

IV. Starting line analysis

V. The Here and Now of FDI in Asia

VI. The New Rule Sets of FDI in Asia

VII. The There and Then of FDI in Asia (2010)

VIII. Cosmic conclusions about the future(s) of FDI in Asia

I: Project overview and introduction

This annotated briefing serves as the Decision Strategies Department (DSD) Report for the Foreign Direct Investment: 3+x(Asia)=Triad2? decision event held in New York City on 16 October 2000.

As of 25 May 2001, this summary brief of the NewRuleSets.Project (both an overview of the project and a summation of the Asian Energy Futures and Foreign Direct Investment events) has been presented on approximately 50 occasions to a variety of Washington think tanks, government agencies, and Wall Street firms. Future briefs are always being scheduled, so contact Tom Barnett directly if you are interested in receiving the brief.

The original draft of the Foreign Direct Investment report was posted on the Naval War College’s web site ) on 9 April 2001. Comments on this final version are welcome from all quarters, but especially from the workshop’s participants and anyone who’s seen the brief in person. Comments should be emailed directly to Tom Barnett, the project’s director (<barnettt@nwc.navy.mil>). He can also be reached by phone at 401.841.4053.

The Foreign Direct Investment event was the fifth in a series of Economic Security Exercises that the DSD has conducted in New York City with the support of Cantor Fitzgerald, the world's largest broker of U.S. Government securities, Eurobonds, and sovereign debt. These events are designed to bring together the worlds of finance and national security to explore issue areas of common interest and, by doing so, build mutual understanding.

For more than 25 years, Cantor Fitzgerald has played a pioneering role as a private-sector intermediary for the fixed income markets. In the early 1970s, Cantor developed the world's first screen-based marketplace for the trading of U.S. government securities. In 1998 it created Cantor Exchange, the first U.S. electronic futures exchange for U.S. Treasury futures. In 1999, Cantor launched a new division known as eSpeed to operate all of its electronic markets. All told, Cantor’s business operations involve financial flows of approximately 50 to 70 trillion dollars a year.

Cantor Fitzgerald provided significant analytic and organizational support to the first three Economic Security Exercises in the series:

- December 1997 event focused on a dual cyber terrorism/disruption of the sea lines of communication (SLOC) scenario involving Wall Street and Southwest Asia, respectively (hard copy of event report is available from the DSD by calling 401-841-1798)

- June 1998 event focused on a dual financial crisis/SLOC disruption in Asia involving Indonesia (hard copy of event report is available from the DSD by calling 401-841-1798)

- May 1999 event focused on the potential global financial repercussions of a substantial Year 2000 Problem (find the report online at ).

eSpeed has stepped to the fore on the NewRuleSets.Project, and serves as Cantor’s support lead for all five of the planned Economic Security Exercises envisioned in this project, beginning with the inaugural Asian Energy Futures event of May 2000 (find the report at <www.nwc.navy.mil/newrulesets/AEFreport.htm>).

The NewRuleSets.Project is a two-and-a-half-year, five-workshop effort designed to explore how globalization and the rise of the New Economy are altering the basic "rules of the road" in the international security environment, with special reference to how these changes may redefine the U.S. Navy's historic role as "security enabler" of America's commercial network ties with the world. Not a data gathering effort, this project lives and dies with the participants we bring together at our workshops—from throughout the global financial and national security communities. The project has five main goals:

- Explore how globalization and the rise of the New Economy are generating new rule sets with regard to how nation-states and national economies interact with one another

- Determine how these new rule sets alter the basic "rules of the road" in the international security environment

- Link these changes in the international security environment to the U.S. Navy's current quest for a "transformation strategy," with special reference to how these changes may redefine the U.S. Navy's historic role as "security enabler" of America's commercial network ties with the world

- Translate these changes in the international security environment into conceptual paradigms of use to strategic planners in the international financial community

- Generally deepen the cross-cultural understanding both sides—the Pentagon and Wall Street—bring to the table during periods of overlapping geo-strategic and geo-economic instability.

Dr. Thomas P.M. Barnett serves as project director. He is currently a Professor/Senior Strategic Researcher in the DSD. Other DSD personnel involved in the project include:

- Prof. Bradd Hayes, Senior Strategic Researcher, DSD

- Dr. Lawrence Modisett, Chairman, DSD

- CDR. Carl Carlson, USN, Deputy Chairman, DSD

- Prof. Gregory Hoffman, Associate Researcher, DSD.

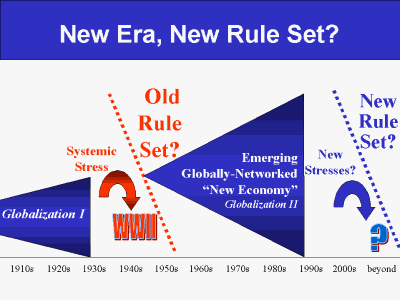

The global rule set that has characterized international relations throughout the Cold War period finds its roots in the systemic stresses of the 1930s—namely, the Great Depression and the rise of fascism in Europe. These twin developments led inexorably to the Second World War, from which sprang the hope that "never again" would the international community allow itself to engage in the sort of economic protectionism that destroyed most of the global economic connectivity achieved by “Globalization I” (roughly, 1870 to 1929).

Based on that "never again" spirit, the postwar Western great powers, led by the United States, attempted to "firewall off" the experiences of the 1930s by creating a new global rule set, whose main attributes were exemplified by such international organizations as the General Agreement on Trade and Tariffs, the UN, the International Monetary Fund (IMF) and the World Bank (WB).

This new global rule set engendered the second great period of economic globalization, creating what we've come to know as the globally networked "New Economy." As this New Economy spreads across the planet, it has suffered significant "growing pains" (e.g., Mexico ’94, Asia ’97-’98, Russia ’98, Brazil ’98-’99), leading some to question whether the postwar rule set is still appropriate for the 21st Century. In other words, as national economies become increasingly intertwined in this information technology-driven New Economy, legitimate questions arise as to whether or not a new global financial architecture is in order and, if so, what it might entail.

While not focusing specifically on any of the ideas currently forwarded by economists for such a new financial rule set, our project takes as its starting premise that the current era will witness great change in the planet’s economy, and that these changes will eventually alter our definitions of national security.

NOTE: A portion of this text is adapted from Thomas P.M. Barnett et. al, Final Report of the Year 2000 International Security Dimension Project, DSD Report 00-5, pp. 15-16, found online at .

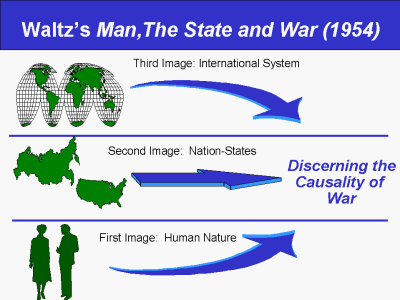

As our starting point for analyzing how an emerging new global economic rule set could alter U.S. definitions of national security, we employ the three-tiered analytic perspective introduced by Kenneth Waltz in his seminal 1954 book on the theory of the causality of war entitled, Man, the State and War (New York: Columbia University Press). Waltz’s approach to this eternal question (“Why do interstate wars start?”) was simply to “view” the matter from three separate perspectives, which he labeled “images”:

- The first image, or “bottom up” perspective, is that of humanity itself, or better stated, human nature. In other words, the question he posed was, is it the essential nature of humanity to engage in violence?”

- The second image, or “straight on” perspective, involves the nation-states themselves. In other words, do certain types of states instigate wars while others do not?

- The third image, or “top down” perspective, involves the all-encompassing international system within which these wars between states occur. In other words, does the current structure (i.e., lacking Thomas Hobbes’ Leviathan, or authoritative enforcer of global order) simply allow or even encourage conflict among states?

In essence, Waltz used these three perspectives to test—or poke holes in—conventional wisdom concerning the presumed complicity of man, states and the international system in fomenting war.

We likewise employ Waltz’s analytical framework in discerning the future of inter-state relations in the post-Cold War era, which we will label the Era of Globalization. We think this three-tiered approach forces a certain discipline to our analysis by pushing us to dis-aggregate the emerging global rule sets according to the “location” of the needs they seek to address—namely, the international system, state governments, or individuals.

NOTE: A portion of this text is adapted from Thomas P.M. Barnett et. al, The U.S. Marine Corps and Non-Lethal Weapons in the 21st Century: Annex A—Alternative Global and Regional Futures, Center for Naval Analyses Quick-Response Report 98-9, September 1998, pp. 2-3.

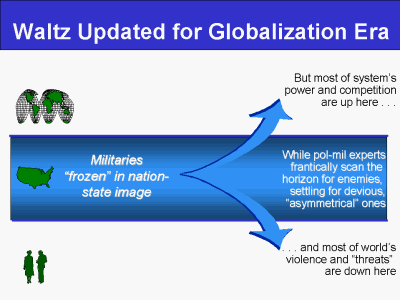

It is our baseline contention that most militaries—but especially the U.S. military—are largely “frozen” in Waltz’s nation-state image. Why so?

In the Cold War, things were fairly straightforward, as both the international system (through blocs) and individuals (through ideologies) were kept in strict subordination to the state-centered superpower conflict. So when the Pentagon looked abroad, all it saw was "us" and "them" states, with that pesky nonaligned gang in between. The focus on states remains to this day. We call it the "Willie Sutton effect," after the famous bandit who, when asked why he robbed banks, replied, "Because that's where the money is." In other words, nation-states have long served as the preeminent collection point (i.e., taxes) for collective security efforts (militaries), but that has begun to change.

The United States has not yet adjusted its state-centered defense policy to account for the two biggest security trends of the globalization era:

- Power and competition have shifted upward, from the state to the system (in the form of the global economy, culture, and communications grid).

- Violence and defense spending (e.g., small arms races, private security firms) have shifted downward, from the state to the individual.

- Worldwide state defense spending and arms transfers are down dramatically from Cold War peaks, leaving some observers to wonder if the U.S. military is being disintermediated from the global security environment—namely, the perception that it is both irrelevant to the rising market of system perturbations (e.g., financial crises) and largely impotent in responding to the booming market of civil strife. While this is a decidedly harsh judgment, we think it’s important to consider the possibility that the U.S. military is—in effect—losing its market share as global security is transformed by the New Economy.

NOTE: A portion of this text is adapted from Thomas P.M. Barnett, “Life After DODth or: How the Evernet Changes Everything,” U.S. Naval Institute Proceedings, May 2000, p. 48.

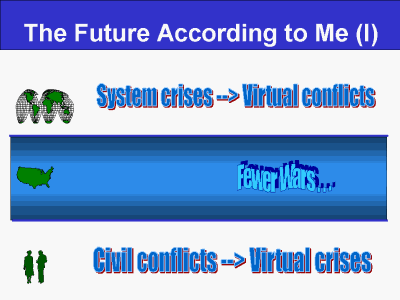

Our take on the future stems from our appreciation of the different trends we see unfolding across the three Waltzian perspectives. First and foremost, we see a future of fewer interstate wars. The early 20th century's high volume of state-on-state warfare will not carry over into the 21st. Nuclear weapons ended great power-versus-great power warfare back in 1945, and as John Keegan predicts, the future belongs far more to civil strife than traditional war.

However, on the international system level we’ll see the U.S. government focusing a lot of diplomatic attention on trying to keep systemic crises—usually triggered by financial tumults—from blossoming into real conflicts among states. Much of this future potential for system-based conflict arises from threats to the global information infrastructure (GII). We get only the slightest hint of this possible future through the emergence of worldwide computer viruses such as the “Love Bug” virus of early 2000. For now, such disruptions seem relatively minor, and since no focused motivations lie behind the acts, little danger is perceived. But it only makes sense that as Information Age economies become increasingly dependent on the movement of raw data, much as Industrial Age economies depended on the movement of raw materials, system-based conflict will be characterized by focused and well-motivated attacks on GII functioning. In short, this is a growing market.

In comparison, real conflicts below the level of the nation-state (i.e., civil strife) should remain fairly constant in the future. Globally there have been a good three to four dozen conflicts every year since World War II that generate 1,000 or more casualties. And while these conflicts are real, U.S. interests tend to be virtual, affording us the flexibility to choose the ones we want to deal with (e.g., Bosnia) and to turn a blind eye to those we don't (e.g., Rwanda).

NOTE: A portion of this text is adapted from Barnett, “Life After DODth,” p. 51.

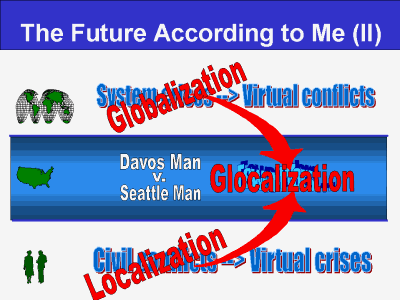

So where can a military fit in this new global environment, where almost all the important crises are either too global or too local for most states to tackle with military force? In a world featuring both integrating globalization (i.e., we are all drawn together by the Internet, transportation, mass media, e-commerce, etc.) and dis-integrating localization (so why then do so many societies and economies seem to be coming apart at the seams?), the great challenge facing governments is fostering compromises between the two, otherwise known as glocalization—adapting the local to the global in ways that improve the former's living standards.

Naturally, this can be fairly contentious, with many societies resisting what Thomas Friedman calls "revolution from beyond” (see his The Lexus and the Olive Tree; New York, Farrar Straus Giroux, 1999). In many societies, globalization is looked upon as forced Americanization, and frankly, that’s too much for most people to swallow. Localization, then, becomes a largely anti-Western rejection of the social homogenization fueled by globalization. In turn, any rejection of globalization constitutes a rejection of the concept of a single global rule set, meaning you tell the world, “Hey, in this corner of the planet we do things differently!” You can call it “Asian values,” or “Chinese characteristics,” but in effect you’re just saying that local identity still matters, even as your region may increasingly embrace globalization and all the social and political change that it ultimately forces.

In short, glocalization is the containment of the Globalization Era—sort of a dot.communism, love it or leave it. This individual choice, made again and again in societies throughout the world, will define the ideological conflict of this age: Davos Man (globalization) versus Seattle Man (localization).

NOTE: A portion of this text is adapted from Barnett, “Life After DODth,” pp. 49-50.

All of the published analytic output connected with the NewRuleSets.Project is available online at the Naval War College’s web site at the following address: http://www.nwc.navy.mil/newrulesets.

The web site provides a Project Summary, which we will update on a regular basis as the multi-year research effort unfolds.

For each decision event, such as the Foreign Direct Investment event, we will post three products:

- Read-ahead package that details the event from a procedural standpoint

- Copy of the brief slides

- Event report, such as this annotated briefing.

The web site also offers links to various related sites:

- Naval War College

- Center for Naval Warfare Studies

- Decision Strategies Department

- Biographies of NewRuleSets.Project personnel

- eSpeed.

The web site also offers direct email to project director Tom Barnett for the purposes of commentary and feedback.

The Foreign Direct Investment event is the second of at least five Economic Security Exercises we plan on conducting for the NewRuleSets.Project. Our current schedule is as follows:

- Asian Energy Futures (conducted 1 May 2000)

- Foreign Direct Investment (conducted 16 October 2000)

- Special Decision Event with the National Intelligence Council (conducted 6 December 2000 at the Center for Strategic Studies, Alexandria VA)

- Asian Environmental Solutions (planned for 4 June 2001)

- Special Decision Event with the Naval War College Foundation Board of Trustees (planned for 14 June 2001)

- Food and water resources (tentatively Fall 2001)

- Critical assets of the New Economy (tentatively Spring 2002).

Beyond the June 2001 events, the schedule is tentative and subject to change. We may also add additional events as the research warrants.

Each of the decision events—unless otherwise noted—will occur in one of two places:

- Windows on the World conference center, World Trade Center, New York City

- Decision Support Center, McCarty-Little Hall, U.S. Naval War College, Newport, Rhode Island.

If you or someone you know is interested in attending one of these events (space is extremely limited), please feel free to contact project director Tom Barnett with your nominations.

Each of the decision event workshops involve roughly thirty participants drawn equally from the financial community, the political-military community, and the regional expert community. The point of the effort is not to amass the most impressive collection of focused subject-matter experts, but to bring together a diverse array of experts, decision makers, and opinion leaders from both the public and private sectors, and let the synergy of their intellectual interactions serve as the fundamental analytic output. In short, the goal of our workshops is a "clash of paradigms," and not a rigorous forecasting effort.

These decision events typically unfold over four to five major sessions. Each session involves both facilitated discussion by the group as a whole and individual participation in collective brainstorming tasks, in which we employ a decision software system known as GroupSystems. Using GroupSystems, each participant enters ideas anonymously via a dedicated laptop, while simultaneously commenting on each other’s inputted ideas asynchronously via a portable Local Area Network, or LAN. In effect, then, we intersperse facilitated discussion with a LAN equivalent of a "chat room" where we explore numerous specific ideas in greater detail.

II: The Asian Energy Futures key findings

The following five slides summarize the decision event report we published concerning our first workshop in the series, Asian Energy Futures. This report is found online at .

The following individuals participated in this workshop:

- Dr. David Baldwin, Columbia University

- Mr. Jim Bishop, Caithness Energy

- Mr. Jim Caverly, Department of Energy

- VAdm. Arthur Cebrowski, USN, U.S. Naval War College

- Dr. Alberto Coll, Center for Naval Warfare Studies

- Capt. Dave Duffie, USN, Council on Foreign Relations

- Dr. Dennis Eklof, Cambridge Energy Research Associates

- Mr. Mike Feeley, Sino-American Development Corporation

- Adm. William Flanagan, USN (ret.), Cantor Fitzgerald

- Dr. Ellen Frost, Institute for International Economics/National Defense University

- Mr. Doug Gardner, eSpeed

- Dr. Philip Ginsberg, Cantor Fitzgerald

- Dr. David Gordon, National Intelligence Council

- Under Secretary of the Navy Jerry Hultin

- Dr. David Jhirad, Department of Energy

- Cdr. Mark Montgomery, USN, National Security Council

- Mr. Roy Nercesian, Poten Partners

- Dr. Minxin Pei, Carnegie Endowment for International Peace

- Mr. Robert Randolph, U. S. Agency for International Development

- Dr. Leif Rosenberger, U.S. Pacific Command

- Amb. Paul Taylor, Center for Naval Warfare Studies

- Dr. Katsuaki Terasawa, University of Mississippi

- Mr. Neal Wolkoff, New York Mercantile Exchange

- Mr. Lundy Wright, Morgan Stanley Dean Witter.

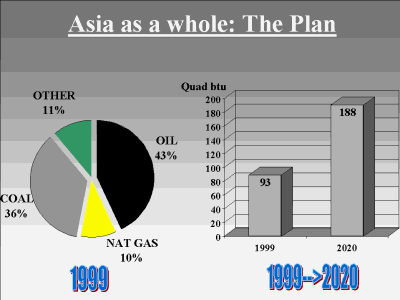

Asia as a whole currently uses about as much energy as the United States, or about 100 quadrillion Btu. By 2020, however, Asia will roughly double its energy consumption while U.S. consumption rises just over a quarter. Asia’s plus-ups are significant no matter what the energy category:

- Oil increases by roughly 88 percent

- Natural gas, 191 percent

- Coal, 97 percent

- Nuclear, 85 percent when Japan is included, but 178 percent when it is not

- Hydroelectric/renewable, 109 percent.

Of the hydrocarbons, Asia comes close to self-sufficiency only in coal. Natural gas is a far different story. This year Asia will use around 10 trillion cubic feet, with Japan, South Korea and Taiwan representing the lion’s share of consumption. These three already buy up virtually all of the region’s currently available methane. The trick is this: Asia’s demand for natural gas skyrockets to 25 trillion cubic feet by 2020, with the vast bulk of the increase occurring outside of that trio. So if those three countries already buy what’s available in-region, that means the rest of Asia will have to go elsewhere—namely, the former Soviet Union and the Middle East.

Asia currently burns about as much oil as the U.S., or roughly 20 million barrels/day (mbd). Since oil is mostly about transportation nowadays, and Asia’s looking at a quintupling of its car fleet by 2020, there is a huge swag placed on this projection. The Department of Energy’s latest forecast is roughly 36 mbd, but even that means Asia has a whole has to import an additional 12 mbd from out of region, or roughly double what it imports today from the Persian Gulf region.

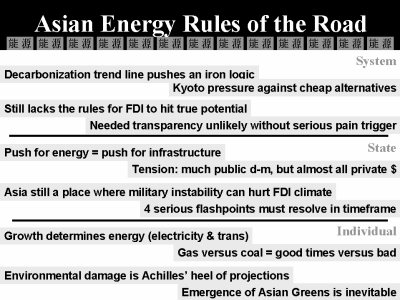

We foresee a series of "rules of the road" emerging for Asia’s energy future.

On the system level:

- We note the decarbonization trend line of human history, moving from wood to coal to oil to methane to hydrogen. Complementing that trend—in an aggregate sense—is the Kyoto Protocol on greenhouse gases, which encourages movement "down" that trend line, even as the CO2 regulatory regime allows some to trade "up" or "down," depending on assigned ceilings and means to purchase additional allowances from others.

- There is the perceived "catch 22" between Asia’s need for large amounts of FDI and the resistance many countries display regarding the transparency Wall Street and other super-markets require for the sort of long-term faith required in infrastructure investments.

On the nation-state level:

- We note the crux of the entire Asian energy problem set: all that infrastructure development will primarily entail private sector money, but too much of the decision making will be performed by government bureaucrats—never a great combination in Wall Street’s opinion.

- It’s also important to remember that Asia is a region still beset by powerful inter-state rivalries and some particularly complex political-military flashpoints that can sour the FDI climate with some alacrity. The four key sources of instability in the coming decade will be: Pakistan-India, China-Taiwan, the Koreas, and Indonesia.

On the individual or subnational level:

- We note that much of the predicted energy growth will depend on individual consumption and usage patterns connected to appliances, electronics, and car transportation. Moreover, the choice to fuel all that electricity demand is often a by-product of economic times, with gas being an easier choice when times are good and coal a last resort when times are hard.

- Finally, workshop participants, while disagreeing on the extent to which green movements would arise in Asia over the coming decades, all agreed that environmental damage (especially health-related concerns from poor air quality) would prove to be an important constraint on many countries’ energy ambitions—unless greater attention was paid to this collective good.

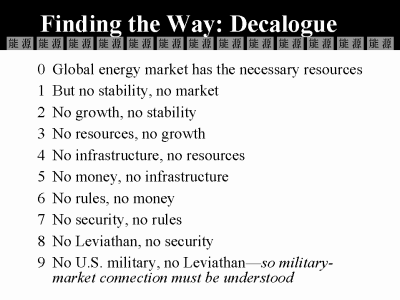

The following Decalogue describes how Asia achieves its ambitious energy development plans by 2020*:

- The starting-point proposition is that the world possesses more than enough resources to accommodate Asia’s energy growth requirements. There is enough coal, oil and gas to make all those projections come true, and they all exist in sufficient amounts right on the Eurasian continent. So it’s not the resources themselves that are in doubt here, just the economic and political transactions required to move them from A to B.

- Along those lines, so long as the markets work, the resources will flow, but the markets require a certain amount of stability—a sense that economic relationships will pay off over the long haul.

- The biggest input to stability is continued economic growth across the Asian market. Populations have been placed on steep consumption trajectories, and expectations of "better days ahead" widely instilled. So long as things progress, no matter how slowly, stability is likely to remain.

- The energy resources are the key to future growth patterns. The only energy Asia has in abundance is coal, whereas oil and gas must come largely from out of region to accommodate future growth requirements.

- The movement of all this energy into the region will require great infrastructure development, especially as the region shifts ahead to greater natural gas use.

- All that infrastructure development will necessitate large amounts of foreign direct investment—of the long-term variety.

- That money will not flow in sufficient amounts unless Western financial institutions see sufficient transparency, accountability, and rule of law.

- That general transparency stems first and foremost from an overarching sense of security across the region. When countries feel threatened, they necessarily become more opaque to the world at large, erecting more firewalls between themselves and the outside they fear.

- Because serious rivalries still exist across the region, and because multilateral security arrangements are non-existent compared to Europe, the region’s closest thing to a Leviathan is the bilateral security relationships most major players currently possess with the U.S.

- If you remove the U.S. military from Asia, you negate the U.S.’s ability to play Leviathan, and thus threaten the underlying security upon which all this development ultimately depends. Right now the U.S. provides the lion’s share of the collective good of Asian security. It is, in many ways, our main export to the region.

* This slide is presented in an article by Thomas P.M. Barnett, "Asia’s Energy Future Requires U.S. Naval Presence," Proceedings, forthcoming.

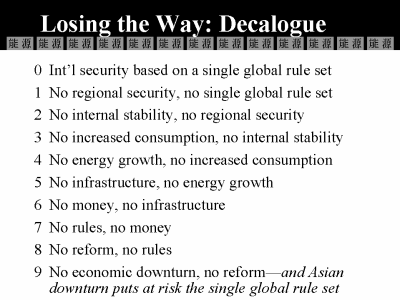

How Asia fails to achieve its ambitious energy development plans by 2020:

- The starting-point proposition is that the current global security system is based on universal adherence to—or at least deference to—a single global economic rule set. For most of the last century, the world was divided into two competing rule sets, but that basically ended with the fall of the Soviet Bloc. Now, only a single rule set remains (capitalism), although philosophical struggles remain about the Anglo-Saxon model of capitalism.

- The single global rule set ends if Asia becomes truly insecure—either internally (state on state) or externally (region versus outside world). If Asia’s regional security collapses, the global rule set collapses along with it, for once Asia’s development path is seen as unique, then markets will work one way in Asia and another way elsewhere in the world.

- The internal stability of the region’s major states (and key neighbors) is essential to the security of the region as a whole. Six major players—in addition to the U.S.—seek spheres of influence along largely overlapping definitions of national interest (Russia, China, Japan, India, Indonesia, Australia). Instability in a major regional power therefore invites the perception of vacuum, upsetting the region’s sense of a balance of power.

- Increased consumption is a key component of the internal stability of states across Asia.

- Energy growth is required to fuel this consumption growth, defined increasingly by ballooning demands for electricity and transportation requirements. Most of this new energy demand will have to be met with outside resources.

- Moving all this energy into the region requires great infrastructure development.

- All that infrastructure development will necessitate large amounts of long-term FDI.

- That money will not flow in sufficient amounts unless Western financial institutions see sufficient transparency, accountability, and rule of law.

- That level of reform is unlikely in Asia without a serious pain trigger in the formof an economic downturn of major proportions or a broad financial panic that crumbles years of economic advance. So long as states can muddle through without real reform, they will.

- If such an immense pain trigger were to occur, the shock to Asia’s body politic could be profound enough to call into question it’s ability to adhere to the concept of a global rule set. In short, major portions of the regional economy could—in effect—drop out of the rule set for indeterminate lengths of time—a sort of firewall capitalism. At that point, all bets would be off regarding the West’s willingness to finance Asian energy developments.

Looking ahead to long-term outcomes, we generate a quartet of long-range scenarios, or landing paths. The X-Y axis is constructed of two questions:

- What is the balance of the overall energy content?

- High-carb diet = more weighted to coal and oil

- Low-carb diet = more weighted to natural gas and renewables.

- What is the balance of the overall decision-making mechanism?

- State-based strategies = more decision-making control is left to public entities

- Market-based strategies = more decision-making control is left to private entities.

The four scenario titles (generated by our participants) are as follows:

- Pipe Dreams (Low-carb diet + Market-based strategies) reflected the participant’s strong skepticism about such a positive outcome combination. It also captured the consensus opinion that gas pipelines would signal movement in this direction. The skepticism stemmed from the participants’ sense that too much cultural change was needed (and too quickly) to achieve the transparency that would, in turn, trigger a sufficient FDI flow for this outcome to unfold.

- Air Today, Gone Tomorrow (High-carb diet + Market-based strategies) reflected the concern of many participants that an unfettered free-market approach would lead to a spoiling of the "commons"—most notably the air. In short, markets promote cost-cutting behavior and Asia’s path of least resistance here is coal-fired electricity.

- Gaz Kapital (Low-carb diet + State-based strategies) reflected the opinion of most participants that, in many instances, it’ll take a strong state to force the sort of monopolistic approach to infrastructure building that a gas-heavy future would require. So, in effect, participants cited this scenario quadrant as a possible transition stage prior to achieving the preferred Pipe Dreams outcome.

- Coal Day in Hell (High-carb diet + State-based strategies) reflected the pessimism most participants held concerning state-dominated economies with large domestic coal supplies. In effect, they believed the temptation to "burn your own" would be too great for power- consciousness bureaucracies to resist. Naturally, this was seen as the worst possible environmental outcome for states with limited political freedom, since no strong venues would exist to promote the public good.

III: The Foreign Direct Investment Workshop

![]()

We designed the Foreign Direct Investment event with the following goals:

- Generate a "relationship profile" delineating how both Asia and the West must adapt past practices to meet the coming challenges of Developing Asia's huge demand for foreign direct investment (FDI)*

- Explore the key scenario variables and dynamics likely to emerge as Developing Asia's FDI requirements balloon in the coming years, focusing on the need for viable rule sets underpinned by a stable regional security environment

- Determine which political-military instability scenarios present the greatest potential to ruin Developing Asia's FDI climate

- Construct realistic downstream scenarios (covering the next 10 years) capturing Developing Asia's movement toward, or away from, a shared FDI rule set with the world's leading economies (i.e, the Triad of the U.S., EU and Japan "squared" to include a fourth leg—Developing Asia).

The one-day workshop (16 October 2000) was held at the Windows on the World restaurant atop the World Trade Center One. The host for the event was the online securities broker-dealer, eSpeed, represented by Adm. William Flanagan, USN (ret.), Senior Managing Director of the parent company, Cantor Fitzgerald, as well as Dr. Philip Ginsberg, Executive Vice President.

* For the purposes of this decision event, we defined Developing Asia as including: Afghanistan, Bangladesh, Brunei, Cambodia, China (to include Hong Kong and Macau), India, Indonesia, Laos, Malaysia, Maldives, Mongolia, Myanmar, Nepal, North Korea, Pakistan, Philippines, Singapore, South Korea, Sri Lanka, Taiwan, Thailand, and Vietnam. These countries constitute the category of South, East and South-East Asia as defined in the United Nations Conference on Trade and Development’s (UNCTAD) annual World Investment Report, which serves as the source for much of the global FDI data presented in this report.

The Foreign Direct Investment event basically explored, over five substantive sessions, a rough "influence net" model that we constructed to describe the key dynamics of Developing Asia’s ability to attract outside investment and that flow’s long-term impact on the global economy and security environment:

- Concerning "The Blend," we conducted two sessions. In the first session called "Where Asia Gets the Money," participants were asked to determine the likely global pool of FDI stock for the year 2010 and then, through a series of "drill down" votes, determine how much of the total global pool would likely end up in Developing Asia. In the second session called "Energy Case Study," we reviewed the findings from the Asian Energy Futures event and asked participants to brainstorm reasons why state governments in Developing Asia should play a lesser or larger role in developing the energy sector.

- Concerning "The Players," we conducted one session called "Build Your Own Free Trade Zone." This voting process was based on the same logic of "connectivity" that fuels the popular movie trivia game known as Six Degree of Kevin Bacon, or The Kevin Bacon Game. In this effort, we asked participants to build three separate free trade zones, and then, by comparing the three groups, drew some conclusions about which Developing Asian states offer the greatest financial connectivity to the region as a whole.

- Concerning "The Unfolding," we conducted two sessions. In the first session called "Pick Your Dream Investment Partner," we had participants brainstorm ideas about what makes Developing Asia more or less attractive as a target for FDI, as well as what makes the U.S., the European Union and Japan more or less attractive as Developing Asia’s sources of FDI. This session was based on the 1960s American television game show called The Dating Game. In the second session called "Scenario Flashpoint," we examined how a future collapse of the North Korean regime would impact the region’s overall FDI climate, with our participants writing advisory emails to various involved political leaders.

- Concerning "The Adjustment," we conducted one session called "Rule Set Scenarios." In this voting process we asked the participants to name and populate—using "Headlines from the Future" —a quartet of long-term FDI climate scenarios for Developing Asia.

All of these participant brainstorming and voting sessions were captured by the GroupSystems software program for our subsequent analysis, along with our notes of the accompanying discussions. Collectively, this material forms the basis for the analysis we present in this report.

The following individuals participated in the day-long workshop:

- Mr. Mark Arens, U.S. Joint Forces Command

- Dr. James Auer, Vanderbilt University

- Mr. Guy Caruso, Center for Strategic and International Studies

- Mr. James Caverly, Department of Energy

- VAdm. Arthur Cebrowski, USN, U.S. Naval War College

- Mr. Thomas Cunningham, Emcor Group

- Dr. Peter Dombrowski, Center for Naval Warfare Studies

- Mr. Mike Feeley, Sino-American Development Corporation

- Adm. William Flanagan, USN (ret.), Cantor Fitzgerald/eSpeed

- Dr. Philip Ginsberg, Cantor Fitzgerald/eSpeed

- Mr. Jeffrey Goetz, Poten and Partners

- Dr. David Harries, Waterpeople Inc./Maccaferri Consulting

- Mr. Russell Hayward, Dynamic Strategies Asia

- Mr. Jeff Huang, Golden Calf Capital

- Dr. Gary Hufbauer, Institute for International Economics

- RAdm. Michael McDevitt, USN (ret.), Center for Strategic Studies/CNA

- Mr. Edward McDougal, Lehman Brothers

- RAdm. Barbara McGann, USN, U.S. Naval War College

- Mr. Jim Miller, Hagler Bailly

- Deputy Under Secretary of the Navy Charles Nemfakos

- Dr. Minxin Pei, Carnegie Endowment for International Peace

- Mr. John Pike, Zentrale Commerzbank AG

- Dr. Jonathan Pollack, Center for Naval Warfare Studies

- Mr. Lucian Pugliaresi, LPI Consulting Inc.

- Ms. Smita Purushottam, Ministry of External Affairs (India)/Weatherhead Center

- Dr. Leif Rosenberger, U.S. Pacific Command

- Ms. Elisabeth Scheper, Netherlands Org. for Internat’l Cooperation/Weatherhead Center

- Capt. Peter Swartz, USN (ret.), Center for Strategic Studies/CNA.

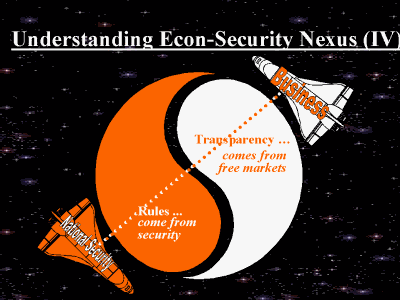

This graphic serves as both table of contents for the presentation of analysis and as a rough theoretical model for the NewRuleSets.Project as a whole.

On the question of the future of foreign direct investment in Asia, we break the process down into five distinct stages (moving from left to right across the graphic):

- We begin with the Here and Now time period, which encompasses the Starting Line environment (i.e., current global FDI market), the inevitably larger flows of FDI from the major global sources to Developing Asia (Triad to Quad?), and the dialectical relationship between the size of the global FDI Pie (i.e., do global FDI flows slow or speed up?) and how much of that global pool actually makes it into Developing Asia (Do the Math).

- Moving from the Here and Now into New Rule Sets, we describe the transition point as a sort of Dating Game between Developing Asia’s three great external "suitors" (North America, Europe, Japan), using this paradigm to explore notions of what makes for an "attractive" long-term FDI relationship.

- In the New Rule Sets time period, rather than trying to present an all-encompassing theoretical model of how various potential pathways unfold, we offer instead a "black box" model, or Scenario Dynamics Grid that displays a matrix listing the key economic, political, technological, cultural, environmental, and security dynamics involved in Developing Asia’s effort to attract FDI. As a dialectical expression of those scenario dynamics, we define the evolution of Developing Asia’s FDI environment as a struggle between the forces of transparency (New Laws) and the region’s continuing inability to move away from Old Orders, or that which keeps Asian capitalism an idiosyncratic model of the global brand.

- Moving from the New Rule Sets to the There and Then, we describe the transition point as a series of Tipping Points, or paradigm shifts that we think Asia must undergo before being able to achieve its maximum potential as a global magnet for FDI.

- In the There and Then time period, we present an X-Y axis with four major outcome scenarios, or Landing Paths, fleshing this framework out with a a series of possible sign posts (projected newspaper headlines) for both positive (Good Signs) and negative (Bad Signs) outcome scenarios. We wrap up this model with The Kevin Bacon Game, which has us exploring the concept of which Developing Asian economies are the "most connected" players in the global FDI game.

We begin our analysis with the Starting Line.

IV: Starting Line Analysis

This slide shows where FDI sits within the universe of financial flows into and out of Developing Asia (1999) and demonstrates why we chose to focus on just direct investment as we looked ahead to the region’s economic future. First, let’s break down the numbers:

Developing Asia self-finances to the tune of about 40 to 50 percent of its investment needs. So when these countries need money, they can basically count on one another for roughly half of it. The rest of their external net financing comes primarily from three main sources: Japan, the EU and the United States. In 1999, the net flow was approximately $40 billion.

Of that $40 billion, almost three-quarters came from private sources, while just over a quarter came from government entities. This breakdown gives you a sense of the relative importance of the private sector versus the public sector.

On the public side of the ledger, very little actually flowed from the International Financial Institutions (IFIs) such as the International Monetary Fund or World Bank. Most (over 90 percent) originated from bilateral aid agencies such as the U.S. Agency for International Development. These numbers give you a sense of the relatively narrow role played by IFIs.

On the private side of the ledger, there was a large outflow of credit, or previously loaned funds. This flow represents several countries (e.g., South Korea, Malaysia) paying back loans that were extended to them during the Asian Flu of 1997-98. Most of this money was loaned by commercial banks.

Also on the private sector side, there was a huge inflow of equity investments. A small portion of that focused on portfolio investments, or the region’s stock markets, but the vast bulk of that flow involved direct investments—meaning foreign entities actually purchasing assets or existing firms.

We chose to focus on FDI because it is usually more strategic and long term in nature, typically involving transnational corporations or small and medium-sized companies setting up overseas operations. Whereas portfolio investments and loans are far more volatile, FDI reflects the global investment community’s appreciation of the region over the long haul. Also, unlike loans, stocks, or foreign aid, FDI involves actual ownership, meaning it is a far less liquid form of investment suggesting cross-border economic integration.

Here we look more closely at the relative importance of public sector foreign aid (ODA, or Official Developmental Aid from the Organization of Economic Cooperation and Development, or OECD) versus FDI for emerging markets.

During the Cold War, ODA substantially outpaced FDI as a source of external financing for developing economies. Even as late as 1990, ODA flows were roughly double that of FDI. In that economic paradigm, IFIs like the World Bank and bilateral donor agencies like USAID were major players in deciding which developing economies would receive the most attention.

This paradigm was turned on its head quite rapidly over the course of the 1990s, suggesting a very different, or new rule set regarding external financing of emerging markets. By the end of the decade, FDI was routinely outpacing ODA by a five-fold margin, effectively pushing the IFIs and bilateral agencies to the margins of the developing world—or to the truly undeveloped economies. Meanwhile, transnational corporations (TNCs) became the great arbiters of the designation "emerging," for TNC-fueled direct investment now represents the largest component of external resource flows to developing countries. According to the United Nations, the world’s average annual FDI outflow for the late 1990s (1995-99) was four times as large than a decade earlier (1985-89).* Simply put, FDI is now one of the most powerful variables of the global economy.

* All references to United Nations figures on FDI are drawn from the UN Conference on Trade and Development’s (UNCTAD) World Investment Reports, various years. Global FDI outflows for the years 1995-99 averaged $540 billion compared to $136 billion for the years 1985-89.

In this slide we explain why we chose to focus on FDI stock (i.e., the accumulated total) versus annual flow.

The chart above compares the net flow of portfolio investments, loans, and FDI into Developing Asia over the 1990s. Looking at stock investment and loans, it is not hard to spot the Asian Flu of the late 1990s, as both lines suffered significant—and in the case of loans, severe—net outflows following its onset.

But looking at the annual flow of FDI, it is not at all apparent that any financial crisis occurred in the region in the 1990s. So while Developing Asia experienced some genuine volatility in both stocks and loans, FDI flows expanded smoothly across most of the decade. This means that at the end of the 1990s, an enormous accumulation of FDI had been achieved by Developing Asia. Unlike loans that have to be paid off at some point, or stock market flows that reverse at a moment’s notice, FDI represents a long term stake—something to be protected by the foreign firm that has put its money on the line.

We chose to focus on FDI stock because we think the accumulation of such direct investment in Asia’s economic future represents that region’s genuine integration into the global economy—a process so huge and unprecedented that it generates new rules for globalization as a whole. Simply put, by accepting long term foreign investments, Asia puts itself on a pathway of accommodating its particular economic rule set to that of the larger international economic community, represented here by Europe and the U.S.

Now let’s look at the distribution of global FDI stocks by source (outward) and target (inward) regions.

Looking first at the inward stock, we get a sense of where TNCs like to invest, or which countries do the best job of attracting outside investors. What the world is really saying to your country when it invests directly in your economy is this: "We like your future market and we want to be a more permanent part of your success." In short, it is a seal of approval or a sign of long term confidence in a country’s internal rule set.

As the numbers above make clear, four regions of the world attract the vast majority of FDI (just over 90 percent):

- Europe (39%)

- North America (25%)

- South/East/Southeast Asia (17%)

- South America (10%).

Who are the great sources of that FDI? Here we look at outward stock totals and see that only three regions register in the double digits:

- Europe (53%)

- North America (28%)

- South/East/Southest Asia (15%).

What this charts makes abundantly clear is this: if Asia has to turn to the former Soviet bloc and the Middle East for energy, it has to turn to Europe and North America for the financial resources to make it happen.

V: The Here and Now of FDI in Asia

Having completed our cursory tour of the FDI landscape, let’s turn our attention to the unfolding of the Here and Now, which we define as the inevitable expansion of the current Triad of global FDI holdings (i.e., United States, European Union, Japan) into a downstream expression which we dub the future Quad (namely, the Triad + Developing Asia).

The concept of the Triad comes from UNCTAD’s 1999 World Investment Report, which described the concentration of global FDI stock in the U.S., Western Europe, and Japan as constituting a special, longstanding stronghold in the global financial community.*

* See UNCTAD, World Investment Report 1999: Foreign Direct Investment and the Challenge of Development (New York: United Nations, 1999), p. 22.

We like to describe the Triad as the financial embodiment of George Kennan’s Cold War strategy of containment, which focused on the U.S. denying the socialist bloc hegemony over Western Europe and Japan. Obviously, we succeeded in more ways than one, for not only did we deny the Soviets an opportunity to divide and conquer the West militarily, we likewise laid the cornerstone for the second great era of globalization by extensively linking these three pillars through foreign direct investment.

Not surprisingly, this chart likewise displays the two strongest bilateral military relationships in the international security environment:

- NATO, or the U.S. and Europe

- The U.S.-Japan security alliance.

In other words, FDI follows the flag even more than trade, because FDI represents long term relationships of trust, and these grow most easily between members of stable military alliances.

The Triad of the U.S., the EU and Japan constitute just over two-thirds of the world’s GDP. In this first snapshot of the Triad’s FDI holdings, we include the European Union’s intra-EU investments, which are sizeable. When we do so, the Triad’s share of global FDI outward stock is 80 percent.

Looking within the Triad itself, we recognize the EU as the largest source of FDI at just over half. But this snapshot is a bit misleading, for as the EU continues its process of integration, counting France’s FDI in Germany gets to be a little bit like counting Michigan’s FDI in Wisconsin. In this report, what really interests us is the amount of the West’s FDI assets that are available for cross-regional flows—namely, into Developing Asia.

We gain a better sense of the relative weight of each leg of the Triad when we exclude the European Union’s intra-EU FDI. By lopping off that large amount from the EU’s FDI total (roughly half), we see that the Triad’s share of global GDP and FDI are equal. In this snapshot, it is easier to identify the United States as the world’s largest source of cross-regional FDI resources.

In this and subsequent calculations, we will include the European Union’s intra-EU investments because, for the foreseeable future, the EU remains an entity far closer to a multinational economic union than a federated state like the United States. This approach also (frankly) allows us to use UNCTAD’s FDI data without having to constantly estimate the intra-EU share.

Proceeding in this manner, we estimate the global FDI stock at $5.7 trillion as of October 2000. If the Triad holds four-fifths of that total, they control an aggregate pool of $4.6 trillion. Using the relative shares established by Snapshot A (EU = 55%, U.S. = 35%, Japan = 10%), we thereby estimate each leg’s holdings as follows:

- EU, $2.6 trillion, with roughly half invested within the EU itself

- United States, roughly one and a half trillion

- Japan, approximately $400 billion.

It is interesting to note that the Triad’s members each have their own little financial sphere of influence with regard to FDI. UNCTAD’s World Investment Report 1999 (p. 22) identified those countries in which the Triad "dominates," meaning those economies in which one of the Triad’s members accounts for "at least 30 percent of total FDI inflows during a three-year period."

Not surprisingly, much like security-based spheres of influence, these financial variants are based on geographic proximity and/or past colonial relationships (with one notable exception noted below).

The United States’ financial sphere of influence is centered almost exclusively on Latin America:

- Latin America = Argentina, Bolivia, Chile, Columbia, Costa Rica, Venezuela, Mexico, and Trinidad and Tobago

- Southeast Asia = Singapore (the noted exception).

The EU’s sphere of influence is clearly bifurcated between regional neighbors and former colonies:

- Former colonies = Brazil, Peru, Cape Verde, Egypt, Swaziland, Tunisia and India

- Regional neighbors = Czech Republic, Hungary, Poland and Turkey.

Japan’s sphere of influence is solely concentrated in Southeast Asia, meaning both neighbors and, in several instances, former WWII-era occupied territories:

- Singapore, South Korea and Thailand.

In essence, just as the containment triad represented a political reach extending beyond its immediate membership, its financial counterpart represents an economic whole that’s larger than the sum of its immediate parts.

Now we turn to Developing Asia and what it brings to the table in terms of FDI outward stock.

Developing Asia’s current pool of FDI outward stock is roughly equivalent to that of Japan, or $400 billion. Using the latest UNCTAD data, we estimate that roughly nine-tenths of that total has been invested within the region itself, leaving only a tenth for distribution to the outside world. Of that 10 percent, the large majority goes to the Triad, and only a tiny fraction to emerging markets outside of Asia.

In effect, Developing Asia pretty much looks out for itself in terms of direct investment, and does not stray very far from home. That tendency, in combination with the substantial FDI provided by Japan, means that Developing Asia has limited—up to now—its reliance on Western investors to roughly one-third of its total FDI requirements. As developing regions go, this has been a relatively closed system in terms of Western influence.

As a theme for the Foreign Direct Investment event, we proposed the emergence of a Quad by 2010, meaning:

- European Union (with any new members unlikely to alter its aggregate FDI total in any significant manner)

- North American Free Trade Area (United States, Mexico, Canada)

- Japan

- Developing Asia.

This expansion could be viewed as the next great step in a sort of post-containment strategy designed to:

- Bring Asia into the now-Western dominated community of developed economies

- By doing so, effectively rule out great power warfare in Asia in the same way it has been ruled out among the Triad members.

Such a Quad would be a formidable concentration of economic might, encompassing (as it does today) roughly 85 percent of the global GDP and 90 percent of the global FDI stock.* The individual shares of the Quad’s total FDI pool would be as follows:

- European Union, 55 percent (including its intra-union FDI)

- NAFTA, 30 percent (including its intra-area FDI)

- Japan, roughly 7 to 8 percent

- Developing Asia, roughly 7 to 8 percent (including its intra-regional FDI).

In many ways, the Quad must emerge in practice, if not in form, for Developing Asia to attract the out-of-region FDI it needs over the coming generation.

* The proposed Quad’s current share of global GDP is 85 percent. The GDP percentage shares of NAFTA and the EU would not change appreciably by 2010, while Developing Asia’s would rise slightly from today’s figure and Japan’s would decline slightly. These changes largely stem from demographic changes in Developing Asia (growing) and Japan (shrinking).

Having presented the notions of the Triad and Quad, we can now explain our somewhat cryptic, pseudo-mathematical decision event "formula":

- 3 refers to the Triad of the United States, the European Union and Japan, or what we like to call the financial embodiment of the Cold War strategy of containment, as well as the three main pillars of Globalization II.

- + x(Asia) refers to our proximate thesis that Developing Asia must turn increasingly to these three main sources of foreign direct investment over the coming years if their ambitious plans for economic development and energy consumption are to be realized.

- = Triad2? refers to our ultimate thesis that eventually Developing Asia will combine with the current FDI Triad to form a recognized Quad.

In terms of global financial architecture, this process is arguably the most important dynamic the world will witness over the coming generation. Naturally, new rule sets (e.g., politically codified expressions of consensus economic tenets) will be required for this process to unfold, but new rule sets will also be a downstream effect.

Where security fits in this argument is a complex question. Clearly, security relations between the legs of the Triad are very strong, forming the deep trust that allows these FDI bonds to form. Currently, many political-military analysts and decision makers in the United States are predicting that Asia will be the focus of interstate conflict in the coming decades. For this Quad to come into being, improved security relations within Developing Asia, and among all four legs of the quartet, is a minimum requirement. If the Quad is achieved in any real fashion, it will reduce the potential for great power war both within Asia and between Asia and the outside world to a considerable degree.

In effect, we argue that the primary strategic goal of the West should be to foster the security and economic integration of Developing Asia to the extent that it effectively joins a developed North that is committed to the long-term integration of free markets and democratic societies.

Having laid our vision for the progressive unfolding of the Here and Now, we now explore the dialectic tension between the amount of money the world has available for foreign direct investment and that share of The Pie that actually makes its way to the countries most in need—the so-called emerging markets. In this section, we asked our participants to Do the Math in a two-fold sense:

- Tell us how how much money the world will likely make available for cross-regional FDI flows over the coming decade

- Help us understand how much of that global pool would end up in Developing Asia, which in effect allows us to plot the strengthening and weakening of existing financial relationships both within Asia and between Asia and the outside world.

Before we took any votes on the subject, we presented participants with the following information regarding the explosive growth of global FDI outward stock over the past 20 years:

- In 1980, the global FDI outward stock was approximately half a trillion dollars. This amount represented 5 percent of the global gross domestic product of approximately $10 trillion.

- Over the 1980s, FDI flows averaged $120 billion a year, increasing the global FDI outward stock in 1990 to roughly $1.7 trillion, or 9 percent of the global GDP of $19 trillion.

- Over the 1990s, FDI flows averaged $400 billion a year, bringing the global FDI outward stock total in October 2000 to approximately $5.7 trillion. This amount represents 18 percent of the current global GDP of roughly $31-32 trillion.

In sum, global FDI outward stock has essentially tripled in both of the last two decades, or a ten-fold increase in all from 1980 to 2000. The FDI stock’s percentage share of the global GDP has basically doubled in both of the last two decades, or a 2 to 3 fold increase in total from 1980 to 2000. Annual flows of FDI has increased 10-fold from 1980 to 2000.

The total picture presented by this data suggests that FDI has become a profoundly important variable in the functioning of the global economy, both as an absolute amount and when measured against the world’s economic growth. For example, global outward FDI flows averaged 5 percent of gross fixed capital formation at the Cold War’s end, but rose to roughly 12 percent by 1998.

What we proposed for the next ten years was that the twin patterns (i.e., rough tripling in absolute stock and rough doubling of percentage share of global GDP every decade) would extend themselves one more time. If this were to occur, the global FDI outward stock in 2010 would be approximately $15 trillion, or 36 to 38 percent of expected global GDP. The annual average flow of FDI required to achieve this growth is approximately $900 billion. For comparison’s sake, the 1999 FDI flow was $800 billion, and in 2000 it was $1.1 trillion. The Economist predicts a drop to roughly $800 billion in 2001 (24 February 2001, p. 80).

This slide lays out our four-step process for Doing the Math on the likely growth of FDI inward stock for Developing Asia by 2010:

- Our participants voted on the global total of FDI outward stock for the year 2010. Noting that the current global total was just under $6 trillion, we gave the participants a range of 5 to 15 trillion US dollars (constant), instructing them to pick a whole number.

- Having then determined the Quad’s share of the global total (using the previously established estimate of 90 percent), our participants voted on the percentage share of the Quad’s total that would remain within the quartet, i.e., invested in one another.

- Having established how much of the global total would be kept within the Quad, our participants next voted on the likely distribution of the Quad’s pool among its four members.

- Finally, we determined the likely inward stock of Developing Asia’s FDI for the year 2010 by adding up the estimated FDI stock totals flowing from:

- United States to Developing Asia

- European Union to Developing Asia

- Japan to Developing Asia

- Developing Asia to itself.

The point of this effort was not to come up with the most accurate forecast of FDI flows, but to force the participants to confront their own expectations about the future functioning of the global economy and their assumptions regarding the ability of the West to pull Asia into a closer, more integrated financial relationship.

We begin the process with the first vote on global FDI outward stock in 2010.

Our participants voted for a global FDI stock of $11 trillion, or a rough doubling of the current (October 2000) global stock. Considering the decline of global equity markets since the decision event last fall, this prediction may strike some as still unduly ambitious, despite the resistance of our participants to embrace the notion of another tripling of the stock amount.

Let’s put this vote in some perspective. First off, global FDI annual flows could drop to roughly $500 to 550 billion and still reach the $11 trillion mark, meaning annual flows could average roughly half of 2000’s record flow of $1.1 trillion. So, in many ways, this vote represented a certain pessimism about the future, despite the prediction of a doubling effect.

Secondly, a 2010 FDI stock total of $11 trillion would represent just over a quarter of the predicted global GDP of $41 to 42 trillion—far from a doubling of today’s percentage share of 18 percent.

Finally, as a point of comparison,we note that the Economist Intelligence Unit (EIU) has just published a report (February 2001), entitled World Investment Prospects, which they claim is the first detailed global forecast of FDI flows. In this report, the EIU predicts a global FDI outward stock total of $10 trillion by the year 2005. This would equate to an average annual flow of $900 billion, or a flow roughly 60 percent heavier than what our group of participants predicted.

If the Quad, as we predict, holds 90 percent of the global FDI stock in 2010, then its combined total would be just under $10 trillion. The totals for each leg of the Quad would be as follows:

- NAFTA, 30 percent or $3.0 trillion

- EU, 55 percent or $5.5 trillion

- Japan, 7.5 percent or $750 billion

- Developing Asia, 7.5 percent or $750 billion.

Having voted on the size of the global FDI "pie" for the year 2010, we next asked our participants to determine the likely share of the Quad’s total FDI outward stock that would remain within the quartet. In effect, we asked them to think ahead to how much the Quad members would choose to concentrate their FDI in one another vice the rest of the world.

In preparation for this vote, we informed participants that the Triad members currently keep approximately two-thirds of their pooled FDI outward stock within the Triad itself (i.e., invested in one another and, in the case of the EU, within the Union itself).

We also reminded participants that, on average, Developing Asia states invest upwards of 90 percent of their outward FDI flows in one another.

In this vote, we asked participants to make a number of simultaneous decisions:

- How the current distribution within the Triad’s three legs would change with the addition of Developing Asia

- How much Developing Asia might redirect its FDI outward toward other Quad members versus how much it would likely keep for itself

- How much remaining FDI each member of the Quad would employ outside the quartet, or to the rest of the world (e.g., Latin America, former Soviet bloc, Southwest Asia, Africa).

Accounting for Mexico and Canada in NAFTA’s total.

In this second vote, our participants voted to keep roughly 80 percent of the Quad’s predicted 2010 FDI stock pool of $10 trillion within the quartet, or approximately $8 trillion. This represents a higher percentage of concentration than that currently seen within the Triad, but that only makes sense given the tremendous economic opportunity represented by Developing Asia over the coming decade, and the fact that Developing Asia adds roughly 4 billion people to the mix.

After deciding how much of the Quad’s FDI total will remain within the quartet, we asked the participants to decide how the pool would likely be distributed among the four legs over the next decade. In effect, we asked them to think ahead to how much the Quad members would choose to concentrate their FDI in Developing Asia vice the other legs—and the rest of the world.

In preparation for the third vote, we informed participants of the current breakdown in FDI stock percentages for each leg of the Triad:

- The strongest bond obviously exists between Europe and the United States, as both direct over 90 percent of their in-Triad FDI total to one another.

- In contrast, neither the EU nor the United States seems able to achieve much direct investment in Japan, which, by all descriptions, throws up a lot of formal and informal barriers to inward FDI flows.

- Japan’s outward FDI is the most evenly distributed within the Triad, with approximately two- thirds going to the U.S. and one-third to the European Union.

In many ways, it is fair to describe the Triad as an incredibly strong dyad with a third leg that clings to both.

Finally, we reminded our participants that Developing Asia currently directs only a small fraction of its FDI outward flows to developed economies.

The one thing we did not provide the participants were current estimates of each Triad members FDI flows to Developing Asia, preferring to let them "guesstimate" those flows on their own.

This last vote was the most complex of the three, but in many ways, all we were asking the participants to do was to tell us which dyad relationships within the proposed Quad would grow stronger in terms of FDI flows over the next decade and which would grow weaker.

Rather than present percentages here, we delineate which dyad relationships grow stronger (measured against today’s estimated percentage shares) over time and which grow weaker.

For NAFTA, the participants voted for stronger dyads with all three Quad partners, meaning less FDI available for the rest of the world. The same basic judgment was offered for the European Union.

In Japan’s case, the group voted for a stronger FDI relationship with only the EU, envisioning a smaller percentage of Japan’s FDI flowing into North America (presumably because it is hard to imagine us investing any less in Japan given how little we do today) and Developing Asia. As a result, a greater share of Japanese funds would be made available for the world outside the Quad (e.g., former Soviet bloc, Mideast, Latin America).

As for Developing Asia, the group basically predicted an opening up of the region’s heretofore "closed" FDI loop, meaning far higher percentage flows to all other Quad legs, as well as to the world outside.

We believe we can draw three basic conclusions from this vote:

- Even a strong reorientation of Western investment toward Developing Asia is unlikely to weaken the already formidable trans-Atlantic FDI bond.

- A strong reorientation of U.S. investment toward Developing Asia may weaken some of our financial connectivity with Japan, in large part because they do not yet allow us into their economy in a meaningful way.

- A strong reorientation of Western investment toward Developing Asia is likely to free up Asia FDI for redirection to other parts of the world.

In sum, when the West invests in Asia it helps to integrate that region into the global economy on two levels: by tying the West closer to Asia and by tying Asia closer to the rest of the world.

Having completed our three "drill down" votes, we are now able to calculate our workshop’s estimate for the likely available inward stock of FDI in Developing Asia in the 2010 timeframe. This calculation is not presented as a "scientific forecast"—something better obtained from an industry group or The Economist Intelligence Unit—but rather as a bias-revealing vote by a cohort of experts covering the issue from political, economic and security angles.

A second point to remember about this calculation is the timing of the vote in relation to market trends. As of mid-October 2000, the market decline was already in full swing, although the full extent of the bear market was not yet in view. Accordingly, it is fair to say that this group vote was not taken by those still caught up in the so-called high-tech bubble of 1998-2000, nor by those unduly depressed by the markets’ rapid decline in the first half of 2001. Nonetheless, this entire voting scheme must be viewed as nothing more than the collective opinion of some smart people one morning in the fall of 2000.

Using our "drill down" voting process, we finally arrive at the following estimated figures for inward FDI stock available to Developing Asia in the year 2010.

Not surprisingly, our participants predicted that Developing Asia itself would provide the largest share of FDI, or between 35 to 40 percent of the total amount of $1.45 trillion. NAFTA would provide the second largest amount at just over a third of a trillion, then the EU with just over a quarter. Japan and the rest of the world would combine to provide approximately $300 billion, or one-fifth.

How do we interpret this combined estimated total of $1.45 trillion FDI inward stock for Developing Asia in 2010?

First, we note that Developing Asia typically accounts for roughly half of the FDI flows into Emerging Markets. So if we double $1.45 trillion to get a $2.9 trillion total for all Emerging Markets, that would represent a 26 percent share of the global total ($11T) the group voted for previously. Such a percentage would be in line with historical averages. According to UNCTAD, Emerging Markets have typically garnered one-quarter of global FDI flows over the years.

Second, we will cite the particular vote of Dr. Gary Hufbauer of the Institute of International Economics, who recently completed a major study on world capital markets.* Hufbauer’s 2010 estimate for all Emerging Markets was $2.9 trillion, or 24 percent of his global FDI stock vote of $12 trillion.

In sum, we believe the participants’ votes are defensible both in terms of fitting within historical ranges and corresponding reasonably well to mainstream economic forecasts. Again, compared to the Economist Intelligence Unit, our group was fairly conservative, but we only expected that since we brought together a fairly wide range of expertise to discuss both future potential and future problems.

* Wendy Dobson and Gary Hufbauer, World Capital Markets: Challenge to the G-10 (Washington DC: Institute of International Economics, 2000).

By any fair estimate, our vote was somewhat rigged. After all, our starting premise for the workshop was Developing Asia’s need to attract more FDI from the West over the coming years to accomplish its ambitious growth targets. So it’s no surprise that our voting process indicated that experts expect more Western investment in Asia in the future.

The question we were really searching to answer here was: How much might the West’s relative financial influence in Developing Asia increase? In effect, if Asia can continue to self-finance to a large degree through intra-Asian FDI, state-based financing, internal savings, and trade surpluses, then the West’s ability to draw Asia toward a single global rule set is limited.

What do we then draw from this session?

- Right now we estimate that the West has cumulatively provided just under a quarter of Developing Asia’s inward FDI stock, compared to the two-thirds that Asian themselves (Japan included) have supplied.

- Based on this voting process, we believe Developing Asia is transitioning to a new reality in which extra-regional providers will come to dominate the FDI market.

- Over the next decade or so, we foresee the West’s position in Developing Asia’s inward FDI stock roughly doubling from its current percentage share.

- While it would be naïve to equate a rough doubling of percentage share with a doubling of financial "influence," it does seem fair to say that the West’s economic influence in Asia will rise dramatically over the coming years as a result of further financial integration brought on by a combination of globalization and Developing Asia’s extraordinary need for foreign investment.

Of course, what cannot be extrapolated from this simple exercise is the answer to the eternal question about the chicken and the egg, which we paraphrase here: Does the West’s rising economic influence lead to the emergence of new rule sets in Asia or must new rule sets arise in Asia for the West’s economic influence to grow?

Where does this vote leave us following the great decline in equity markets in early 2001 and the resulting slowdown in the global economy? How much stock (pun intended) can we place in this sort of projection?

Again, we like to emphasize how modest our group’s projection actually turns out to be when compared to recent history.

Developing Asia ended the 20th Century with an inward FDI stock total of about three-quarters of a trillion dollars. To achieve a 2010 stock total of $1.45 trillion, the region would need to attract around $70 billion a year (counting both intra- and inter-regional flows). $70 billion equates to roughly the average inward flow of the mid-1990s, or substantially less than what poured in during the heyday of the high-tech bubble in stock markets at the very turn of the century.

During this voting process, we took time out at several occasions to ask participants to brainstorm reasons why they might be wrong in their collective guesstimate of $11 trillion in global FDI stock for 2010. This slide presents ten of the best arguments we heard about why there won’t be a larger FDI flow into Developing Asia over this decade.

The arguments can be grouped into four general camps:

- The 1990s were extraordinary, and past performance does not guarantee future results.

- There is a natural ceiling on FDI: at some point more mature market venues appear and investors will prefer them for their increased efficiency and ease

- The global economy is due for some breakdowns, crises, snafus.

- Developing Asia is simply ill-equipped to absorb all this investment without destabilizing outcomes.

Here we present the flip side arguments, or why there very well could be a bigger FDI flow into Developing Asia than we’re envisioning.

The arguments can likewise be grouped into four general camps:

- The global fundamentals are in good shape; this is just a necessary pause in the action.

- Transnational corporations are the big drivers here, and they see a big market they want to be part of (think about a middle class of perhaps a billion people!).

- If there is a natural ceiling on FDI, Asia is a long way away from it, given the immaturity of their financial markets.

- Asia is opening up and working on new rules, so the long term looks very solid.

By presenting these alternative analyses, we give you a sense of the range of opinions that came together in three, very particular votes. In short, we had a full complement of both bulls and bears.

VI: The New Rule Sets of FDI in Asia

Moving to New Rule Sets, we shift gears from number crunching to a norm-oriented brainstorming exercise where we explore the notion of what makes a region an "attractive" FDI partner, in terms of either providing or receiving investment flows.

We dub this workshop session "The Dating Game," after the 1960s American television game show of the same name.

The original version of "The Dating Game" debuted in December 1966 and immediately became a major game show hit on American television.

During its seven-and-a-half year daytime run on the ABC network, earning a distinction as the 31st longest running television game show in history, the program set up some 3,000 dates for contestants. Appearances on the show helped launch the fledgling careers of numerous actors who later became major television and movie celebrities, including Sally Field, Tom Selleck, Burt Reynolds, Arnold Schwarzenegger, and Steve Martin—to name a few.